English

English Français

Français 日本語

日本語 中文

中文Kamoa-Kakula Mining Complex in the Democratic Republic of Congo sold a record 93,812 tonnes of payable copper and recognized revenue of $460 million in Q3 2022

Kamoa-Kakula recorded $940 million in EBITDA for the nine months ended September 30

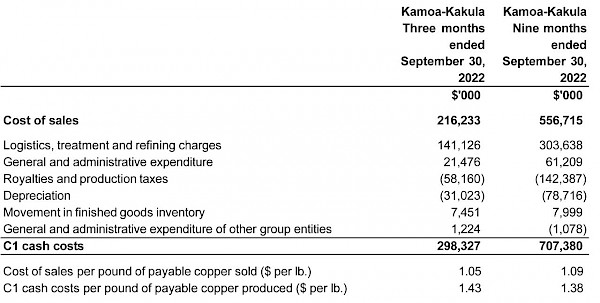

Kamoa-Kakula’s cost of sales total $1.05 per pound of payable copper during the third quarter, with C1 cash costs of $1.43 per pound

Over the first nine months of 2022, Kamoa-Kakula milled approximately 5.1 million tonnes of ore at a 5.6% copper grade, to produce 240,736 tonnes of copper

During September and October, Kamoa-Kakula’s annualized production rate exceeded 400,000 tonnes of floated and filtered copper

Ivanhoe Mines further increases the lower end of Kamoa-Kakula’s 2022 production guidance range to between 325,000 and 340,000 tonnes of copper in concentrate

JOHANNESBURG, SOUTH AFRICA – Ivanhoe Mines’ (TSX: IVN; OTCQX: IVPAF) President Marna Cloete and Chief Financial Officer David van Heerden are pleased to present the company’s financial results for the nine months ended September 30, 2022. Ivanhoe Mines is a leading Canadian mining company developing and operating its four principal mining and exploration projects in Southern Africa: expanding the operations of the world-class Kamoa-Kakula Mining Complex in the Democratic Republic of Congo (DRC); building the tier-one Platreef palladium, rhodium, nickel, platinum, copper and gold development in South Africa; restarting the historic, ultra-high-grade Kipushi zinc-copper-lead-germanium mine in the DRC; as well as exploring the expansive exploration licences of Ivanhoe’s Western Foreland for copper discoveries adjacent to Kamoa-Kakula. All figures are in U.S. dollars unless otherwise stated.

HIGHLIGHTS

- The Kamoa-Kakula Mining Complex produced 97,820 tonnes of copper in concentrate during the third quarter of 2022, up from 87,314 tonnes in Q2 2022 and 55,602 tonnes in Q1 2022. Kamoa-Kakula has produced approximately 274,115 tonnes of copper year-to-date as of October 31, 2022.

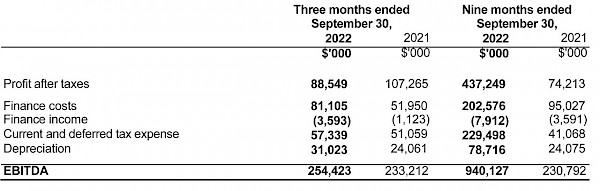

- During the third quarter, Kamoa-Kakula sold 93,812 tonnes of payable copper and recognized revenue of $460.5 million, with an operating profit of $222.8 million and an EBITDA of $254.4 million.

- Kamoa-Kakula’s cost of sales per pound (lb.) of payable copper sold was $1.05/lb. for Q3 2022, compared with $1.15/lb. and $1.08/lb. in Q2 2022 and Q1 2022, respectively. Cash costs (C1) per pound of payable copper produced totalled $1.43/lb., compared to $1.42/lb. and $1.21/lb. in Q2 2022 and Q1 2022, respectively. Cash costs (C1) per pound of payable copper produced for the first nine months of 2022 total $1.38/lb.

- During September and October, Kamoa-Kakula’s annualized production rate was more than 400,000 tonnes of floated and filtered copper, with this rate periodically exceeded over 24-hour periods during the third quarter.

- Kamoa-Kakula’s previously announced de-bottlenecking program is approximately 70% complete and is tracking ahead of schedule. The program, will increase the combined processing capacity of the Phase 1 and 2 concentrator plants from 7.6 million tonnes per annum to approximately 9.2 million tonnes per annum. Once complete in Q2 2023, the rate of copper production is projected to reach approximately 450,000 tonnes per annum.

- Kamoa-Kakula Mining Complex milled approximately 2.1 million tonnes of ore during the quarter at an average grade of 5.6% copper, compared to 2.0 million tonnes of ore at an average grade of 5.4% copper in Q2 2022.

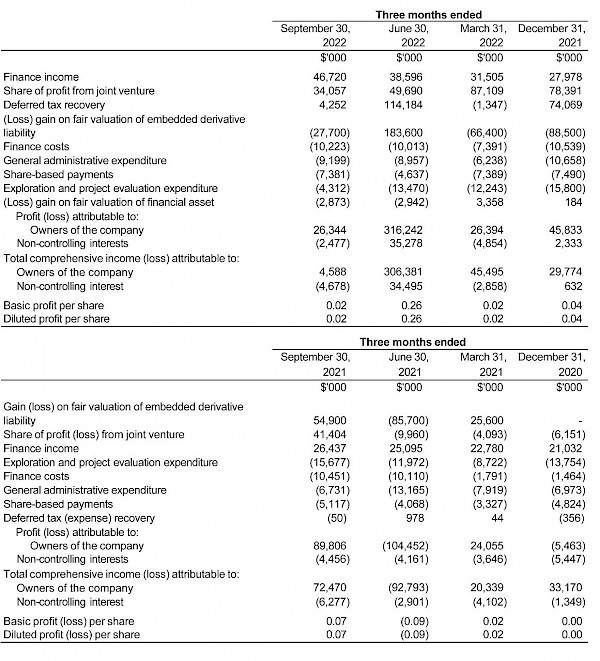

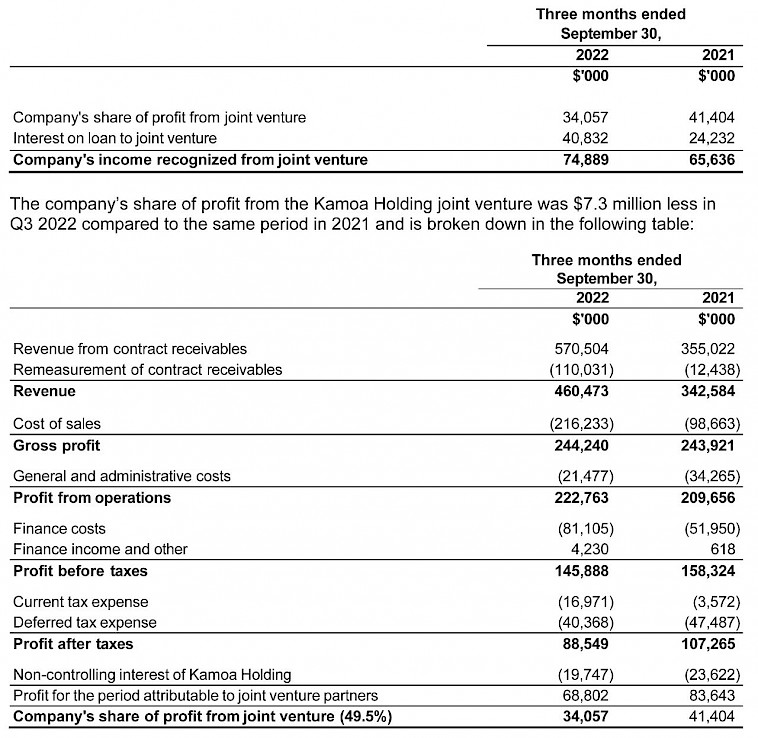

- Ivanhoe Mines recorded a profit of $23.9 million for Q3 2022, compared with a profit of $351.5 million and $85.4 million during Q2 2022 and Q3 2021, respectively. The quarterly profit includes Ivanhoe Mines’ share of profit and finance income from the Kamoa-Kakula joint venture of $74.9 million for Q3 2022.

- Ivanhoe Mines has a strong balance sheet with cash and cash equivalents of $663.3 million as at September 30, 2022, and expects that Kamoa-Kakula’s operating and expansion capital expenditures on Phase 3 will continue to be funded from copper sales and additional facilities at the Kamoa-Kakula joint venture.

- Ivanhoe Mines further increases the lower end of its 2022 production guidance range for Kamoa-Kakula to between 325,000 and 340,000 tonnes of copper in concentrate following the early commissioning of the Phase 2 expansion.

- Given ongoing cost pressures experienced during the second and third quarters, largely related to logistics costs, the company is tightening its full-year C1 cash cost guidance to between $1.35/lb. and $1.40/lb. (previously $1.20/lb. to $1.40/lb.).

- The basic engineering design for Kamoa-Kakula’s Phase 3 expansion is complete, with the results to be included in the updated technical report that will be released early in the new year.

- Earthworks excavation for the Phase 3 mine, concentrator and direct-to-blister flash smelter is advancing as planned.

- Lateral underground mine development on Platreef’s 950-metre-level, towards the location of the first ventilation shaft position, progressed well during the quarter. More than 300 metres of lateral development has been completed since work commenced in April 2022.

- Construction of Platreef’s first solar-power plant commenced during the quarter, with commissioning expected in the second half of 2023. The solar-generated power from the plant will be used for mine development and construction activities, as well as for charging Platreef’s battery-powered underground mining fleet.

- After quarter end, Ivanhoe Mines was granted 80 square kilometres of new, highly prospective exploration rights, known as the “Mokopane Feeder”, adjacent to the company’s Platreef Project in the Bushveld Complex, South Africa.

- In September 2022, Ivanhoe Mines and Gécamines hosted a breaking-ground ceremony at the Kipushi mine, marking the start of surface construction activities.

- Early works in preparation for the start of underground mining at Kipushi were completed in August 2022. This included the refurbishment of key mining excavations, as well as blasting of the truck tip turning bay and truck passing bays on the 1,150-metre-level.

Full-year 2022 production and cost guidance revised

Management anticipates that the early commissioning of the Phase 2 concentrator plant in April 2022, approximately four months ahead of schedule, as well as the strong operating performance to date, has enabled Kamoa-Kakula to further increase the lower end of its full-year 2022 production guidance from a range of between 310,000 to 340,000 tonnes of copper in concentrate, to between 325,000 and 340,000 tonnes.

Given ongoing cost pressures experienced during the second and third quarters, largely related to logistics costs, the company is tightening its full-year C1 cash cost guidance to between $1.35/lb. and $1.40/lb. (previously $1.20/lb. to $1.40/lb.).

Cash costs (C1) is a non-GAAP measure used by management to evaluate operating performance and includes all direct mining, processing, and general and administrative costs. Smelter charges and freight deductions on sales to the final port of destination (typically China), which are recognized as a component of sales revenues, are added to C1 cash cost to arrive at an approximate cost of delivered finished metal.

Ivanhoe Mines’ President Marna Cloete commented:

“This is an incredibly transformational time for Ivanhoe Mines as construction activities advance at Kamoa-Kakula’s Phase 3 expansion and smelter, as well as at Platreef and Kipushi. We aim to build on the impressive track record we’ve developed from Kamoa-Kakula, where both Phase 1 and 2 were constructed on budget and ahead of schedule.

“I am extremely proud of the operating team at Kamoa-Kakula, who have continued to exceed expectations and are on track to meet the upper end of our original full-year production guidance.

"Alongside the majority of the mining industry, we have experienced inflationary pressures throughout this year. These pressures have been mostly logistics-specific, as Kamoa-Kakula’s on-site costs have been well managed and stable. Great progress has been made by the team at Kamoa-Kakula, working with our joint-venture partners, offtake partners and the Democratic Republic of Congo government, in implementing initiatives to remove the logistical bottlenecks experienced during the year. We expect to reap a positive impact from this hard work over the coming quarters.

“Our team remains focused on the strong value-creation opportunities in our project pipeline and I believe we’ll emerge stronger than ever following this period of global volatility. We are extremely confident in copper’s mid- to long-term fundamentals as the world navigates the transition to clean energy.”

Ivanhoe Mines to host a conference call for investors on November 14

The company will hold an investor conference call to discuss the Q3 2022 financial results at 10:30 a.m. Eastern time / 7:30 a.m. Pacific time on November 14. The conference call dial-in is +1-416-764-8650 or toll-free 1-888-664-6383, quote “Ivanhoe Mines Q3 2022 Financial Results” if requested. Media are invited to attend on a listen-only basis.

Link to join the live audio webcast: https://app.webinar.net/YvWzpn3maEn

An audio webcast recording of the conference call, together with supporting presentation slides, will be available on Ivanhoe Mines’ website at www.ivanhoemines.com.

After issuance, the Financial Statements and Management’s Discussion and Analysis will be available at www.ivanhoemines.com and www.sedar.com.

Principal projects and review of activities

1. Kamoa-Kakula Mining Complex

39.6%-owned by Ivanhoe Mines

Democratic Republic of Congo

The Kamoa-Kakula Mining Complex, operated as the Kamoa Holding joint venture between Ivanhoe Mines and Zijin Mining, has been independently ranked as the world’s fourth-largest copper deposit by international mining consultant Wood Mackenzie. The project is approximately 25 kilometres west of the town of Kolwezi and about 270 kilometres west of Lubumbashi. Kamoa-Kakula Mining Complex’s Phase 1 concentrator began producing copper in May 2021 and achieved commercial production on July 1, 2021. The Phase 2 concentrator, which doubled nameplate production capacity, was commissioned in April 2022.

Ivanhoe sold a 49.5% share interest in Kamoa Holding Limited (Kamoa Holding) to Zijin Mining and a 1% share interest in Kamoa Holding to privately-owned Crystal River in December 2015. Kamoa Holding holds an 80% interest in the project. Since the conclusion of the Zijin transaction, each shareholder has been required to fund expenditures at Kamoa-Kakula in an amount equivalent to its proportionate shareholding interest. Ivanhoe and Zijin Mining each hold an indirect 39.6% interest in Kamoa-Kakula, Crystal River holds an indirect 0.8% interest, and the DRC government holds a direct 20% interest.

Kamoa-Kakula took delivery of new large-scale underground equipment (MT65 haul truck and ST18 Scooptram) from Epiroc of Norsborg, Sweden. The new equipment aims to assist in improving underground productivity.

Health and safety at Kamoa-Kakula

At the end of September 2022, Kamoa-Kakula reached 2.46 million work hours free of a lost-time injury and had a Total Recordable Injury Frequency Rate (TRIFR) (total injuries recorded per 1,000,000 hours worked) of 1.73 for the nine months ended September 30, 2022.

Kamoa-Kakula regretfully reported a fatal accident in September 2022. The fatal accident occurred in a development area at the underground Kansoko Mine when a fall of ground struck a Kamoa-Kakula employee. Kamoa-Kakula is undertaking a comprehensive internal investigation into the accident and is working with the DRC authorities to facilitate their investigation of the accident. Kamoa-Kakula continues to strive toward its workplace objective of zero harm to all employees and contractors.

The projects construction team at Kamoa-Kakula conducted in-depth, onsite training on advanced risk assessment techniques through an accredited training institution. A group of 120 managers, supervisors and safety officers participated in the training program.

Kamoa-Kakula summary of operating and financial data

|

Q3 2022 |

Q2 2022 |

Q1 2022 |

Q4 2021 |

|

| Ore tonnes milled (000’s tonnes) |

2,082 |

1,950 |

1,083 |

1,059 |

| Copper ore grade processed (%) |

5.60% |

5.44% |

5.91% |

5.96% |

| Copper recovery (%) |

85.9% |

84.0% |

87.1% |

86.4% |

| Copper in concentrate produced (tonnes) |

97,820 |

87,314 |

55,602 |

54,481 |

| Payable Copper sold (tonnes) |

93,812 |

85,794 |

51,919 |

53,165 |

| Cost of sales per pound ($ per lb.) |

1.05 |

1.15 |

1.08 |

1.12 |

| Cash cost (C1) ($ per lb.) |

1.43 |

1.42 |

1.21 |

1.28 |

| Sales revenue before remeasurement ($’000) |

570,504 |

699,381 |

467,453 |

458,880 |

| Remeasurement of contract receivables ($’000) |

(110,031) |

(205,248) |

52,142 |

29,656 |

| Sales revenue after remeasurement ($’000) |

460,473 |

494,133 |

519,595 |

488,536 |

| EBITDA ($’000) |

254,423 |

286,313 |

399,391 |

357,619 |

| EBITDA margin (% of sales revenue) |

55% |

58% |

77% |

73% |

All figures in the above tables are on a 100%-project basis. Metal reported in concentrate is before refining losses or deductions associated with smelter terms. This release includes EBITDA, “EBITDA margin” and "Cash costs (C1) per pound” which are non-GAAP financial performance measures. For a detailed description of each of the non-GAAP financial performance measures used herein and a detailed reconciliation to the most directly comparable measure under IFRS, please refer to the non-GAAP Financial Performance Measures section of the Q3 2022 MD&A.

C1 cash cost per pound of payable copper produced can be further broken down as follows:

|

|

|

Q3 2022 |

Q2 2022 |

Q1 2022 |

Q4 2021 |

| Mining |

($ per lb.) |

0.41 |

0.39 |

0.30 |

0.27 |

| Processing |

($ per lb.) |

0.12 |

0.14 |

0.15 |

0.17 |

| Logistics charges (delivered to China) |

($ per lb.) |

0.56 |

0.51 |

0.36 |

0.37 |

| Treatment, refining and smelter charges |

($ per lb.) |

0.21 |

0.21 |

0.20 |

0.24 |

| General and administrative expenditure |

($ per lb.) |

0.13 |

0.17 |

0.20 |

0.23 |

| C1 cash cost per pound of payable copper produced |

($ per lb.) |

1.43 |

1.42 |

1.21 |

1.28 |

C1 cash costs are prepared on a basis consistent with the industry standard definitions by Wood Mackenzie cost guidelines but are not measures recognized under IFRS. In calculating the C1 cash cost, the costs are measured on the same basis as the company’s share of profit from the Kamoa Holding joint venture that is contained in the financial statements. C1 cash costs are used by management to evaluate operating performance and include all direct mining, processing, and general and administrative costs. Smelter charges and freight deductions on sales to the final port of destination, which are recognized as a component of sales revenues, are added to C1 cash cost to arrive at an approximate cost of delivered, finished metal. C1 cash costs exclude royalties and production taxes and non-routine charges as they are not direct production costs.

Copper C1 cash costs per pound of payable copper for the second and third quarters of 2022 remain elevated by approximately 17% and 18% respectively compared with the first quarter. This is mostly due to an increase in logistics charges experienced in transporting Kamoa-Kakula’s copper concentrate. The site costs, however, have been much less affected by inflation year-to-date. The cost of sales for the quarter were $1.05/lb., compared with US$1.15/lb. and US$1.08/lb. in Q2 2022 and Q1 2022, respectively.

Kamoa-Kakula undertaking optimization of logistics costs

Kamoa-Kakula and other regional operators have experienced delays and increased logistics costs due to a shortage of available trucks, border congestion and occasional work action by truck drivers. Kamoa-Kakula is working alongside its offtake partners, Zijin Mining, CITIC Metal and Trafigura, as well as the government of the DRC, to undertake initiatives to optimize the transportation of Kamoa-Kakula’s products.

These initiatives include working with Kamoa-Kakula’s offtake partners, logistics service providers and local entrepreneurs to increase regional trucking capacity, improve processes for clearing products for export and the opening of new border crossings between the DRC and Zambia. Kamoa-Kakula is also continuing to explore the optionality of using a greater number of ports for exporting concentrate. These include Durban in South Africa, Dar es Salaam in Tanzania, Walvis Bay in Namibia and Beira in Mozambique, and longer-term the port of Lobito in Angola.

Cost pressures associated with logistics have occurred since Kamoa-Kakula’s Phase 2 concentrator declared commercial production four months ahead of schedule in early Q2 2022. While concentrate production doubled, this was not met with a sufficient supply of trucking capacity and this led to an increase in trucking contractor market pricing. In addition, the Lualaba Copper Smelter was closed in June for maintenance. This further increased trucking demand.

Under normal operating conditions, the cycle time of trucking concentrate from the mine gate to the port of Durban, and back, is approximately 45 days. Congestion experienced in the past two quarters saw this cycle time increase to as high as 70 days. This, in turn increased trucking demand by an additional 50%, further pushing up trucking contractor market pricing. The cycle time is shorter for the ports of Dar es Salaam, Walvis Bay and Beira.

Two new commercial DRC-Zambia border crossings opened, helping to reduce logistics bottleneck

During September, the operating hours of the Kasumbalesa border, located in Haut-Katanga province, were increased from 6 hours to 12 hours. The extended operating hours are expected to be permanent. Earlier in the quarter, congestion at the Kasumbalesa border crossing saw extended queues, which caused delays in customs clearing. Delays from congestion often incur additional charges.

During the third quarter, two new commercial border crossings opened on the DRC-Zambia border. A border crossing at Sakania, located approximately 150 kilometres by road southeast of Kasumbalesa, opened for commercial exports and imports. In addition, the Mokambo border crossing, located half way between Kasumbalesa and Sakania opened for commercial imports.

Reopening of Lualaba Copper Smelter in September reduces trucking demand

The Lualaba Copper Smelter, located approximately 50 kilometres from the Kamoa-Kakula Mining Complex, completed its scheduled maintenance in early September and the transportation of copper concentrates to the facility recommenced shortly thereafter. While undergoing scheduled maintenance, Kamoa-Kakula’s concentrate production was wholly transported and exported as a copper concentrate (approximately 50% contained copper), without the expected quantity of blister copper (approximately 99% contained copper), thereby temporarily increasing logistics volumes and costs for the quarter. The restart of the Lualaba Copper Smelter will assist in reducing overall shipping volumes, as the export of blister copper incurs lower logistics costs per unit compared to copper concentrate. The Lualaba Copper Smelter is expected to treat approximately 120,000 tonnes of copper concentrates from Kamoa-Kakula in 2022.

The increased opening hours of the Kasumbalesa border crossing, the opening of a new commercial export border crossing at Sakania, the resumption of blister copper shipments from the Lualaba Copper Smelter, as well as increased availability of trucks, is expected to ease congestion over the coming quarters.

A step-change improvement in cash costs of between 10% and 20% is anticipated once the Phase 3, 500,000-tonne-per-annum, direct-to-blister flash smelter is commissioned, expected by the end of 2024. A significant part of the reduction in cash costs, on a per tonne basis, is a result of the trucks hauling ~99% pure blister copper, instead of ~50% contained copper concentrate. Therefore, truck demand for hauling copper products to port is expected to decrease from current levels once the smelter is in operation. In addition, the smelter will generate valuable by-product credits from the sale of sulphuric acid, which is in structural deficit in the DRC Copperbelt.

Kakula Mine optimization work targeting grades towards 6% copper

Ongoing mining optimization work at the Kakula Mine successfully targeted higher head grades during the third quarter, to increase head grades up to 6% copper. Kamoa-Kakula continues to evaluate additional material handling capacity at the Kakula Mine to increase mining rates to feed the de-bottlenecked Phase 1 and 2 processing capacity of 9.2 million tonnes per year. Further details will be incorporated into the Phase 3 expansion pre-feasibility study, scheduled for release early in 2023.

While the near-term expansion of underground infrastructure at Kakula takes place, ore is being drawn from the surface stockpiles to maximize copper production as the Phase 1 and 2 concentrators are currently operating at more than design capacity. As of the end of September 2022, Kamoa-Kakula’s high- and medium-grade ore surface stockpiles totalled approximately 4.2 million tonnes at an estimated grade of 4.15% copper for a total of over 174,000 tonnes of contained copper.

Installation of additional underground conveying capacity at the Kakula South decline will increase the output of ultra-high-grade ore to the surface from the Kakula mine.

Record quarterly production of 97,820 tonnes of copper in Q3 2022

Kamoa-Kakula’s Phase 1 and 2 concentrator plants milled approximately 2.1 million tonnes of ore during the third quarter at an average feed grade of 5.6% copper, up from 1.95 million tonnes at an average grade of 5.4% copper in the second quarter. This included high-grade, run-of-mine ore from the Kakula Mine, supplemented with ore from the surface stockpiles to meet the throughput over design capacity. In line with design parameters, copper recoveries averaged approximately 86% during the quarter.

The Kamoa-Kakula Mining Complex set a new quarterly production record in the third quarter of 2022, with 97,820 tonnes of copper in concentrate produced, up from 87,314 tonnes produced in the second quarter and 55,602 tonnes produced in the first quarter. Kamoa-Kakula produced a total of 240,736 tonnes of copper in concentrate in the nine months ending September 30, 2022. Subsequent to quarter end, during the month of October Kamoa-Kakula produced a further 33,379 tonnes of copper.

The Phase 1 and 2 milling and flotation circuits continue to operate in excess of design capacity. At the end of October, there was also an additional 5,786 tonnes of floated, but not yet filtered, copper in the circuit. This marks the second month in a row that floated and filtered copper production from the Kamoa-Kakula Mining Complex has exceeded 400,000 tonnes per annum on an annualized basis.

The difference between floated, and subsequently, filtered copper arises from the current bottleneck in concentrate thickening and filter capacity at the tail end of the processing circuit. Excess floated copper is currently being temporarily stored as a slurry in a fully-lined pond adjacent to the Phase 1 and 2 concentrators. The unfiltered copper in inventory will be reclaimed into the concentrate thickener and filter press once capacity is expanded following the installation of a new concentrate thickener and Larox filter press, as part of the ongoing de-bottlenecking program.

All figures are on a 100% project basis and metal reported in concentrate is before refining losses or deductions associated with smelter terms. Guidance involves estimates of known and unknown risks, uncertainties and other factors, which may cause the actual results to be materially different.

Phase 1 and Phase 2 debottlenecking project to boost throughput to 9.2 million tonnes of ore per year is tracking ahead of schedule

Kamoa-Kakula’s previously announced de-bottlenecking program is approximately 70% complete and is tracking ahead of schedule. The program will increase the combined design processing capacity of the Phase 1 and 2 concentrator plants from 7.6 million tonnes per annum to approximately 9.2 million tonnes per annum

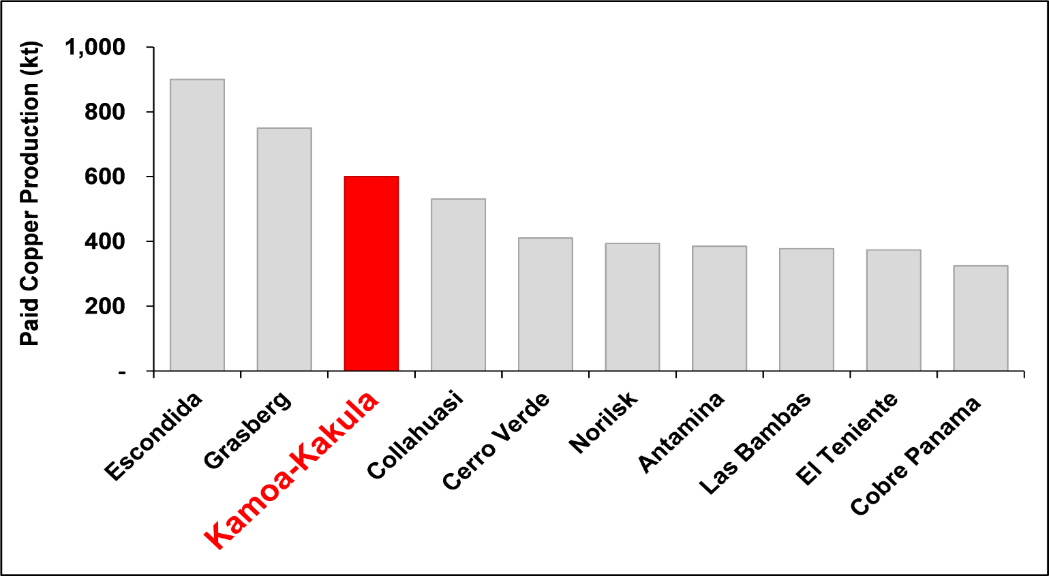

The de-bottlenecking program is targeting completion in the second quarter of 2023 and will boost Kamoa-Kakula’s annual production to approximately 450,000 tonnes of copper in concentrate by the second quarter of 2023, positioning Kamoa-Kakula as the world’s fourth largest copper producer.

Figure 1: Kamoa-Kakula’s base-case, pro-forma Phase 3 copper production (after de-bottlenecking of Phase 1 and 2 is complete) relative to the world’s projected top 10 producing mines in 2022 by payable copper production.

Source: Wood Mackenzie (April 2022). Note: Kamoa-Kakula production of 600 kt copper in concentrate is based on expected Phase 1, 2 and 3 steady-state production, following the de-bottlenecking of both Phase 1 and 2 concentrators, and commercial ramp-up of the Phase 3 concentrator.

Civil works on site are effectively complete with structural steel and plate work erection ongoing and electrical and mechanical installation well underway.

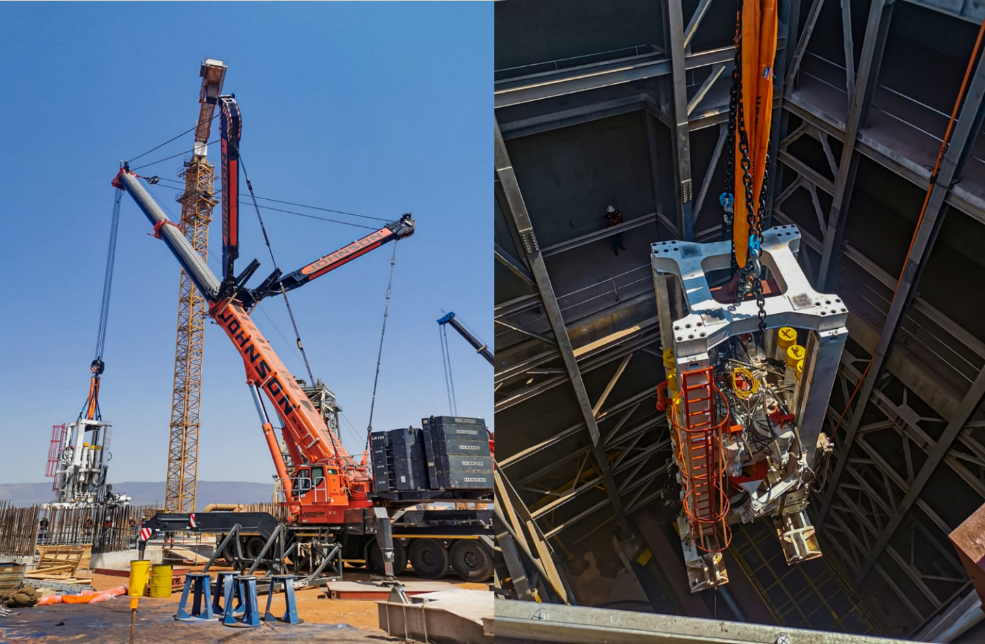

Planned plant shutdowns to install the new equipment required for the de-bottlenecking program are scheduled to take place between December 2022 and January 2023, with the aim to minimize any negative effects on production. Civil works on site are nearing completion with structural steel and plate work erection ongoing and electrical and mechanical installation now underway.

Aerial view of the additional concentrate thickener at Kamoa-Kakula’s Phase 1 and 2 concentrator plants that is under construction as part of the de-bottlenecking program.

Construction is progressing well in advance of the installation of the fourth Larox filter press at Kamoa-Kakula’s concentrate warehouse.

Phase 3 box-cut and basic engineering complete, procurement and construction activities have commenced

Construction of the twin declines to the Kamoa 1 and Kamoa 2 underground mines and excavation to access Phase 3 mining areas is advancing well.

Basic engineering design for the Phase 3 underground mine infrastructure, 5-million-tonne-per-annum concentrator plant and associated infrastructure is now complete. Detailed engineering, procurement and early construction activities are advancing well.

Earthworks for the concentrator plant and surface infrastructure is advancing on schedule, with the contract for the civil construction awarded and site preparation underway. Equipment fabrication is also ongoing.

Tenders for structural steel supply have been received and are in the process of being adjudicated.

Following the commissioning of Phase 3, expected by the end of 2024, Kamoa-Kakula will have a total processing capacity of more than 14 million tonnes per annum. The completion of Phase 3 is expected to increase copper production capacity to approximately 600,000 tonnes per annum. This production rate will position Kamoa-Kakula as the world’s third-largest copper mining complex, and the largest on the African continent (see Figure 1).

Kamoa-Kakula’s Phase 3 expansion includes a 500,000-tonne-per-annum, direct-to-blister flash smelter to produce approximately 99% pure copper metal, and the replacement of Turbine #5 at the Inga II hydroelectric power station. The turbine replacement will supply an additional 178 megawatts (MW) of clean hydroelectric power to the national grid and provide power for Phase 3.

Earthworks at the smelter site situated adjacent to Kamoa-Kakula’s Phase 1 and Phase 2 concentrator plants are approximately 70% complete with civil construction activities currently underway.

Detailed engineering is well advanced with orders for the bulk of the long lead items of equipment placed. Equipment and structural steel fabrication are currently underway.

The Kamoa-Kakula smelter uses technology supplied by Metso Outotec of Espoo, Finland, and meets the International Finance Corporation’s (IFC) emissions standards. The smelter has been sized to process most of the copper concentrate forecast to be produced by Kamoa-Kakula’s Phase 1, Phase 2, and Phase 3 concentrators, while any remaining copper concentrate may be smelted locally.

Located inside a containment area, rebar installation is taking place for the foundations of the acid tanks at the smelter site. The 500,000-tonnes-per-annum direct-to-blister smelter will be the largest single-line flash copper smelter in Africa.

Draw-down of surface ore stockpiles has commenced; stockpiles hold approximately 4.2 million tonnes grading 4.15% copper, containing more than 174,000 tonnes of copper

Kamoa-Kakula’s high- and medium-grade ore surface stockpiles totalled approximately 4.2 million tonnes at an estimated grade of 4.15% copper as of the end of September 2022. The operation mined 1.70 million tonnes of ore grading 5.39% copper in Q3 2022, which was comprised of 1.61 million tonnes grading 5.51% copper from the Kakula Mine, including 0.83 million tonnes grading 6.89% copper from the mine’s high-grade centre.

A total of 118.3 kilometres (73.5 miles) of underground development has been mined across the mining complex at quarter end. While the ongoing expansion of underground infrastructure at the Kakula Mine takes place, ore will be drawn as required from the stockpile to maximize copper production, as the concentrators are currently operating at more than the design capacity.

Inga II long-lead order items under construction and EPC contractor mobilized to the site

In July 2021, Ivanhoe Mines Energy DRC, a sister company of Kamoa Copper tasked with delivering reliable, clean, renewable hydropower to Kamoa-Kakula, signed an addendum of the financing agreement under a public-private partnership with the DRC’s state-owned power company, SNEL, to upgrade a major turbine (#5) at the existing Inga II hydropower facility on the Congo River.

The Inga II turbine #5 refurbishment project is expected to produce an additional 178 MW of renewable hydropower, providing Kamoa-Kakula’s Phase 3 expansion, its associated smelter, as well as future expansions, with sustainably generated electricity. The refurbishment is scheduled for completion in Q4 2024.

Mobilization to the Inga II site took place in October. A health, safety and environment (HSE) survey has been completed and the results have been submitted to SNEL for review.

A new, 6.5-metre diameter, 89-tonne runner, which generates the rotation movement inside Turbine #5, is currently under construction. The bespoke equipment is the longest-lead order of the equipment items being replaced or refurbished at Turbine #5. It is expected that the component will be delivered to the Inga II site at the end of 2023. The new runner design has been engineered to improve efficiency and deliver an additional 16 MW of power generation from Turbine #5, compared with the original design that was installed in 1982.

A study is underway to upgrade the transmission capacity of the existing grid infrastructure between the Inga II hydropower facility and the Kamoa site. The engineering for the remaining equipment items is ongoing and the ordering of the replacement components is expected to be completed early in the new year.

The runner blades for the new turbine are being fabricated at Voith’s fabrication facility in China. Delivery of the completed runner to the Inga II hydropower facility is expected by the end of 2023.

Empowering local communities through sustainable development

Ivanhoe Mines founded the Sustainable Livelihoods Program in 2010 to strengthen food security and farming capacity in the host communities near Kamoa-Kakula. Today, approximately 900 community farmers are benefiting from the program, producing high-quality food for their families and selling the surplus for additional income. Sustainable Livelihoods commenced with maize and vegetable production, and now include fruit, aquaculture, poultry and honey.

The banana plantation project began in 2018 and now consists of 11 hectares of banana trees. The 27 women from local communities who own this project harvested and sold more than 2,830 kilograms of bananas since June 2022.

Construction of additional livestock farming facilities is underway and planned to be completed in October. Together with the aquaculture project – comprised of approximately 140 fishponds with plans for the construction of another 100 new ponds – the livestock farm will significantly contribute toward local entrepreneurship and enhanced regional food security.

Construction of a health clinic at the Muvunda Village has been completed and the facility has now been equipped. The construction of a church at Tshilongo Village is approximately 70% complete.

Implementation of the first regulatory five-year community development plan, the Cahier des Charges, which provides $8.6 million towards educational, healthcare, agricultural, potable water provision, and other initiatives, is well underway. The construction and equipping of two early childhood development centres were finalized and officially handed over to the Provincial Minister of Education in September 2022. These new facilities and curriculum afford access to formative educational programs for the first time in the region. The Mupenda aquaculture project and the Muvunda poultry project also have been launched, and the planning and design of two rural community health centres have progressed well.

Local community enterprise programs such as the brickmaking and sewing programs continued. These businesses have also been expanded, enabling them to ramp-up production, and providing additional income and employment opportunities. A review of the business model for the landscaping and gardening enterprise programs aims to provide a new operating model which will enhance business efficiency and growth.

Bulk earthworks now are underway at the site for the Kamoa Center of Excellence, which once in operation, aims to create a sustainable and community-centered learning environment in the heart of the Democratic Republic of Congo.

A visit by Kamoa-Kakula to the Complexe Scolaire Les Calinours School in Kolwezi, to introduce the high school students to the programs available at the Kamoa Centre of Excellence that opens next year. The application deadline is in December 2022 for enrollment in September 2023. A full bursary program is also available.

The Kamoa Centre of Excellence will be a world-class facility, developed on the outskirts of Kolwezi, offering degrees, diplomas and short courses in collaboration with internationally accredited institutions.

The project will take place over multiple phases to accommodate departments, as well as sports facilities, to be added over time. Initial curriculum offerings will be aligned with the mining industry i.e., mining engineering, French-English language courses, and much more. Phase 1 will include just over 100 students, with enrollment to commence in 2023.

2. Platreef Project

64%-owned by Ivanhoe Mines

South Africa

The Platreef Project is owned by Ivanplats (Pty) Ltd (Ivanplats), which is 64%-owned by Ivanhoe Mines. A 26% interest is held by Ivanplats’ historically disadvantaged, broad-based, black economic empowerment (B-BBEE) partners, which include 20 local host communities with approximately 150,000 people, project employees and local entrepreneurs. A Japanese consortium of ITOCHU Corporation, Japan Oil, Gas and Metals National Corporation, and Japan Gas Corporation, owns a 10% interest in Ivanplats, which it acquired in two tranches for a total investment of $290 million.

The Platreef Project hosts an underground deposit of thick, platinum-group metals, nickel, copper, and gold mineralization on the Northern Limb of the Bushveld Igneous Complex in Limpopo Province – approximately 280 kilometres northeast of Johannesburg and eight kilometres from the town of Mokopane.

On the Northern Limb, platinum-group metals mineralization is primarily hosted within the Platreef, a mineralized sequence traced for more than 30 kilometres along strike. Ivanhoe’s Platreef Project, within the Platreef’s southern sector, is comprised of two contiguous properties: Turfspruit and Macalacaskop. Turfspruit, the northernmost property, is contiguous with, and along strike from, Anglo Platinum’s Mogalakwena group of mining operations and properties.

Since 2007, Ivanhoe has focused its exploration and development activities on defining and advancing the down-dip extension of its original discovery at Platreef, now known as the Flatreef Deposit, which is amenable to highly mechanized, underground mining methods. With Shaft 1, the initial access to the deposit, now in operation and hoisting development rock from underground, Ivanhoe is focusing on construction activities to bring Phase 1 of Platreef into production by Q3 2024.

Health and safety at Platreef

At the end of September 2022, the Platreef Project reached 1,571,130 lost-time injury-free hours worked with a Total Recordable Injury Frequency Rate (TRIFR) (total injuries recorded per 1,000,000 hours worked) of 4.57 for the nine months that ended September 30, 2022.

Surface construction activities underway, while lateral underground mine development progressing well

Underground development work is focused on establishing the waste passes from the 750-metre and the 850-metre levels to the 950-metre level, installing the required underground infrastructure on the various stations, developing towards the first reef and stoping areas, as well as developing towards the first ventilation shaft location. Mine development on the 950-metre level progressed well with more than 300 metres of development completed at the end of Q3 2022.

Construction for Platreef’s Phase 1 concentrator plant has commenced, with the first production on track for Q3 2024. Earthworks construction is now underway, with mill foundation civil activities advancing well. Mill manufacturing is also progressing well, with other long-lead equipment orders placed.

The 10-metre diameter Shaft 2, which will be among the largest hoisting shafts on the African continent, is on the critical path for the future Phase 2 expansion of Platreef. Following the completion of the 26-metre concrete hitch-to-collar construction in August 2022, Ivanplats plans to continue with the construction of the 103-metre-tall concrete headframe that will house the shaft’s 6 million tonnes per annum hoisting equipment. The pilot drilling required for the raised bore centre hole of the shaft and the commencement of the sliding of the headframe are both planned to commence before the end of 2022. This will provide optionality in bringing forward the timeline of Phase 2 production.

Shaft 2 headgear construction preparation advancing well with the batch plant commissioned and required tower cranes erected.

Shaft 2 raise-boring equipment being lowered into position.

Construction of the foundations of Platreef’s Phase 1 concentrator plant is progressing well.

Construction of Platreef’s first solar-power plant commenced in Q3 2022 with commissioning expected in 2023. The solar-generated power from the plant will be used for mine development and construction activities, as well as for charging Platreef’s battery-powered underground mining fleet.

Platreef development currently funded by $300-million stream financing, with efforts to finalize additional senior debt facility well underway

Ivanplats received the second and final prepayment of the $300 million Platreef streaming agreement during the third quarter. In addition, the company signed updated engagement letters with its mandated lead arrangers, Société Générale and Nedbank, to increase the Platreef project senior debt facility from $120 million to $150 million. The expanded facility, which is subject to due diligence, will provide further optionality in terms of project financing, and limit potential equity contributions for Platreef’s Phase 1 development. Discussions continue to finalize the expanded facility with the view to it being completed in the new year.

As announced on December 8, 2021, Ivanplats’ $300 million in stream-financing agreements are with Orion Mine Finance and Nomad Royalty (which was subsequently acquired by Sandstorm Gold Royalties). This includes a $200 million gold-streaming facility and a $100 million palladium and platinum streaming facility. The first prepayment of $75 million was received upon the closing of the transaction in December 2021, with the final $225 million instalment received in September 2022.

The stream facilities are subordinated to any future senior secured financing. Ivanplats remains flexible to raise additional debt or equity and has pre-agreed inter-creditor arrangements with the stream purchasers for future senior debt. The stream facilities are guaranteed by Ivanplats and secured over its assets, as well as Ivanhoe and the Japanese consortium’s shares of Platreef.

The fully realized stream agreements allow Ivanplats to advance Platreef’s ongoing Phase 1 construction activities, with an initial capital cost of $488 million as set out in the Platreef feasibility study announced in February 2022.

Platreef continues to focus on community development, human resources, and job training

Platreef supports several educational programs and provides free Wi-Fi in host communities.

The implementation plan for the second cadetship program, planned for commencement in October 2022, has progressed well, with recruitment and selection almost complete. The cadetship program offers young people from the local community to obtain a National Certificate in Health and Safety, as well as mining competencies, such as utility vehicle operations from the Murray & Roberts Training Academy. The program also aims to enhance gender diversity within the mine’s workforce, striving for an aspirational target of 50% female representatives in the program. Platreef’s first cadetship program provided learnership opportunities to over 50 local students, 54% of whom were female.

Local economic development projects planned in the Social and Labour Plan (SLP) will contribute to community water-source development through the Mogalakwena Municipality boreholes program. Other planned SLP projects, which will be conducted in partnership with other parties, include the refurbishment and equipping of a health clinic in Tshamahansi Village.

Enterprise and Supplier Development initiatives continue to focus on creating capacity and opportunities for local small, medium, and micro enterprises, which play a crucial role in stimulating the regional economy and establishing sustainable job creation in the communities around Mokopane.

Over 60 local small, medium, and micro enterprises have attended an accredited 5-day business accelerator training and the company has initiated additional programs aimed at training local businesses on “How to do Business with Ivanplats”. To date over 100 members of the local small, medium, and micro enterprises have attended, with a further 350 scheduled to attend in November 2022.

A widespread poverty alleviation waste campaign project was initiated in partnership with the Impact Catalyst and the Bonega Communities Trust, Ivanplats’ broad-based black economic empowerment vehicle. Other projects included an awareness campaign for the United Nations’ Sustainable Development Goals in the form of a poster competition in eight primary schools near the mine, as well as a health and hygiene campaign, aimed at keeping young girls from missing school through the donation of sanitary products.

Phillip Ramphisa, Ivanplats’ Environmental Manager, addresses high school students regarding the importance of the U.N. Sustainable Development Goals.

Dr. Poobie Pillay (third from right), Ivanplats’ Enterprise and Supplier Development Manager, with a group of recent local entrepreneurs graduating from the business accelerator training program.

3. Kipushi Project

68%-owned by Ivanhoe Mines

Democratic Republic of Congo

The Kipushi zinc-copper-germanium-silver-lead mine in the DRC is adjacent to the town of Kipushi and approximately 30 kilometres southwest of Lubumbashi. It is located on the Central African Copperbelt, approximately 250 kilometres southeast of the Kamoa-Kakula Mining Complex and less than one kilometre from the Zambian border. Ivanhoe acquired its 68% interest in the Kipushi Project in November 2011, through Kipushi Holding which is 100%-owned by Ivanhoe Mines. The balance of 32% in the Kipushi Project is held by the state-owned mining company, Gécamines.

Kipushi Holding and Gécamines have signed a term sheet for a new agreement to return the ultra-high-grade Kipushi Mine to commercial production. Kipushi will be the world’s highest-grade major zinc mine, with an average grade of 36.4% zinc over the first five years of production.

Health and safety at Kipushi

At the end of September 2022, the Kipushi Project reached a total of 5.43 million work hours free of lost-time injuries with a Total Recordable Injury Frequency Rate (TRIFR) (total injuries recorded per 1,000,000 hours worked) of 1.98 for the nine months that ended September 30, 2022. It has been more than three and a half years since the last lost-time injury occurred at the project.

Project activities underway to return Kipushi to production

In preparation for the start of underground mining, early works activities were completed in August 2022, comprising the refurbishment, and supporting of key mining excavations, as well as blasting of the truck tip turning bay and truck passing bays on the 1,150-metre-level. Explosive storage bays and a trackless machinery assembly bay were also completed. Cover drilling of the main decline commenced in September 2022.

During the third quarter, Ivanhoe and Gécamines hosted a breaking-of-ground ceremony to commemorate the start of the construction of Kipushi’s processing plant. In addition, Ivanhoe signed a memorandum of understanding (MOU) with the provincial government of Haut-Katanga to study options for upgrading the DRC-Zambia border crossing in the town of Kipushi for commercial imports and exports.

Earthworks for the new concentrator are advancing well with civil works just starting, and the first concrete pour took place in October 2022. The bulk of the long-lead items for the concentrator plant have been ordered and manufacturing is underway. The plant is scheduled to be complete by Q3 2024.

Financing and offtake discussions are well advanced with several interested parties and are expected to culminate in combination with a final, revised joint venture agreement between Kipushi Holding and Gécamines.

Underground work at Kipushi is progressing ahead of first production.

The breaking-of-ground ceremony was attended by His Excellency Jean-Michel Sama Lukonde, Prime Minister of the Democratic Republic of the Congo, Her Excellency Adèle Kayinda Mahina, Minister of State and Minister of Portfolio, Her Excellency Antoinette N’Samba Kalambayi, Minister of Mines, members of the provincial government of the Haut-Katanga Province and other national, provincial, and local dignitaries, in addition to representatives from Ivanhoe, Gécamines and the town of Kipushi.

A new commercial border crossing at Kipushi will provide a significant advantage to the Kipushi Mine as a direct means of importing materials and consumables, as well as clearing customs and exporting products from the mine, and will provide socio-economic benefits to the town and Province of Haut-Katanga.

The opening of the Kipushi border crossing also is anticipated to provide ancillary benefits to Kamoa-Kakula, where work is underway to improve processes for clearing copper products for export and to open alternative export border crossings between the DRC and Zambia, to alleviate congestion at the existing border crossings at Kasumbalesa and Sakania in Haut-Katanga Province.

Community enrichment and development

The Kipushi Project has built a new potable water station to provide a free daily supply of water to the municipality of Kipushi. Approximately 1,000 cubic metres of potable water is pumped hourly and continuously to consumers daily.

Another 50 boreholes of potable water are planned to be drilled around the Kipushi district over five years, to reach areas not served by current distribution. In addition to the existing, already drilled and operational 16 boreholes, six new boreholes are being drilled and will be completed before the end of the year to improve community members’ accessibility to potable water around the Kipushi district.

The Kipushi Project continues to support educational initiatives through ongoing renovations at the Mungoti School, and the granting of bursaries and scholarships to local students. Over 300 local beneficiaries are participating in an adult literacy and education program this year after the program resumed with physical classes following a two-year interruption due to the COVID-19 pandemic. The successful program will culminate for the year in the fourth quarter with an official graduation ceremony.

Ivanhoe is committed to fostering access to potable water in the footprint area of our mines. Since 2018, Ivanhoe has installed sixteen solar-powered, fresh drinking water boreholes in communities surrounding the Kipushi Project.

4. Western Foreland Exploration Project

90%- and 100%-owned by Ivanhoe Mines

Democratic Republic of Congo

Ivanhoe’s DRC exploration group is targeting Kamoa-Kakula-style copper mineralization through a regional exploration and drilling program on its Western Foreland exploration licences, located to the north, south and west of the Kamoa-Kakula Project. Western Foreland consists of 17 licences that cover a combined area of approximately 2,407 square kilometres.

Exploration models that successfully led to the discoveries of Kakula, Kakula West, and the Kamoa North Bonanza Zone on the Kamoa Copper SA mining licence, are being applied to the Western Foreland extensive land package by the same team of exploration geologists responsible for the previous discoveries.

At the Makoko West area, drilling is ongoing and mapping of the mafic intrusions in the Kibaran basement is underway. At the Lupemba target area in the far southwest of Western Foreland, ground gravity and a large 800-metre-spaced air core grid were initiated; drilling continued at both the Mushiji prospect, to the north of the Kamoa-Kakula mining licence, and in the Makoko Sud target area.

Regional stratigraphic drilling was completed at the Lupemba licence during Q2 2022, with an 800- by 800-metre air core drill grid initiated over the licence early in the third quarter. The program was intended to drill though the Kalahari sand cover and take a top of saprolite and top of bedrock sample, for geochemical and lithological mapping, respectively. Also, at Lupemba, a ground gravity survey program is in progress, and the results will be used in conjunction with the airborne gravity and air core drilling program to provide increased structural definition around the edge of the basin.

The drilling of the Makoko West area is targeting the westerly extension of the Makoko Sud deposit discovered in 2018. Drilling was aimed at infilling the original wide-spaced drill sections along the strike of the projected Makoko graben feature. The area is characterized by a significant number of north-northeast trending mafic intrusions that disrupt the continuity of mineralization along the trend. To better understand the distribution of the intrusions a stream mapping program was undertaken to the north of the target area to try and map out the individual intrusions.

Two holes were drilled in the Mushiji area three kilometres north of the Kamoa-Kakula licence to define the edge of the Roan sandstone. The first did not intersect any Roan and the second is in progress.

Soil sampling programs were also completed at the Sakanama and 155 locations at Kakula East.

Selected Quarterly Financial Information

The following table summarizes selected financial information for the prior eight quarters. Ivanhoe had no operating revenue in any financial reporting period. All revenue from commercial production at Kamoa-Kakula is recognized within the Kamoa Holding joint venture. Ivanhoe did not declare or pay any dividend or distribution in any financial reporting period.

Discussion of Results of Operations

Review of the three months ended September 30, 2022, vs. September 30, 2021

The company recorded a total comprehensive loss of $0.1 million for Q3 2022 compared to a total comprehensive income of $66.2 million for the same period in 2021.

The company recognized income in the aggregate of $74.9 million from the joint venture in Q3 2022, which can be summarized as follows:

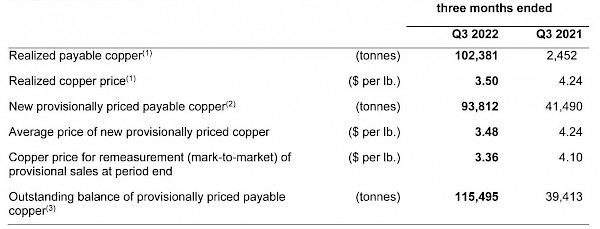

Kamoa-Kakula sold 93,812 tonnes of payable copper in Q3 2022 realizing revenue of $460.5 million for the Kamoa Holding joint venture, compared to 41,490 tonnes of payable copper sold realizing revenue of $342.6 million in Q3 2021. Revenue did not increase in proportion to tonnes sold due to the lower prevailing copper price in Q3 2022. The realized, provisional and copper price used for the production remeasurement (mark-to-market) of provisional sales can be summarized as follows:

(1) Payable copper that was provisionally priced in prior quarters and settled during the quarter.

(2) Provisionally priced payable copper sold is subject to final pricing over the next several months.

(3) Outstanding balance is made up of new provisionally priced payable copper from the current quarter, with the balance from the previous quarter.

Kamoa-Kakula’s other operating data is summarized under the review of operations section.

The company recognized a loss on the fair valuation of the embedded derivative financial liability of $27.7 million for Q3 2022, compared to a gain on the fair valuation of the embedded derivative financial liability of $54.9 million for Q3 2021.

Finance income for Q3 2022 amounted to $46.7 million and was $20.3 million more than for the same period in 2021 ($26.4 million). Included in finance income is the interest earned on loans to the Kamoa Holding joint venture to fund past development which amounted to $40.8 million for Q3 2022, and $24.2 million for the same period in 2021, and increased due to the higher accumulated loan balance.

Exploration and project evaluation expenditure amounted to $4.3 million in Q3 2022 and $15.7 million for the same period in 2021. Exploration and project evaluation expenditure for Q3 2022 related to exploration at Ivanhoe’s Western Foreland exploration licences, while Q3 2021 also included amounts spent at the Kipushi Project, for which expenditure was capitalized in Q3 2022 due to the recommencement of the development of the project.

Review of the nine months ended September 30, 2022, vs. September 30, 2021

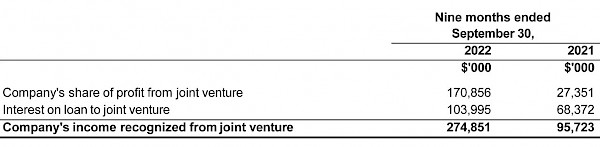

The company recorded a total comprehensive income of $383.4 million for the nine months that ended September 30, 2022, compared to a loss of $13.3 million for the same period in 2021. The profit for the period principally relates to the company’s share of profit from the Kamoa Holding joint venture, the gain on fair valuation of embedded derivative liability and the recognition of the deferred tax asset relating to the Kipushi Project, all three of which are described in greater detail below.

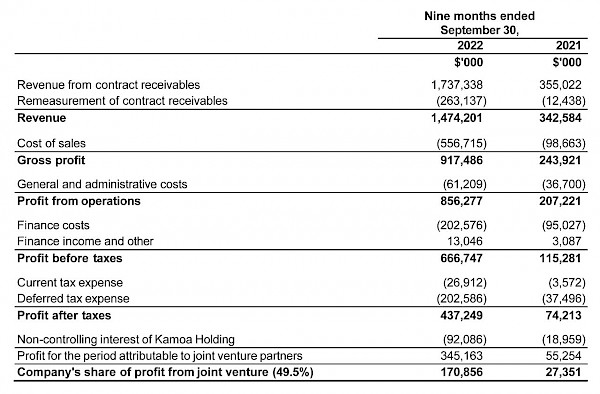

The Kamoa-Kakula Mining Complex commenced commercial production on July 1, 2021, and sold 41,490 tonnes of payable copper until September 30, 2021, realizing revenue of $342.6 million, compared to 231,525 tonnes of payable copper sold in the nine months ended September 30, 2022, realizing revenue of $1,474.2 million for the Kamoa Holding joint venture. Kamoa-Kakula’s other operating data is summarized under the review of operations section on page 4. The company recognized income in aggregate of $274.9 million from the joint venture in the nine months ended September 30, 2022, which can be summarized as follows:

The company’s share of profit from the Kamoa Holding joint venture was $170.9 million in the nine months that ended September 30, 2022, compared to $27.4 million in the same period in 2021. The following table summarizes the company’s share of profit of the joint venture for the nine months ended September 30, 2022, and for the same period in 2021:

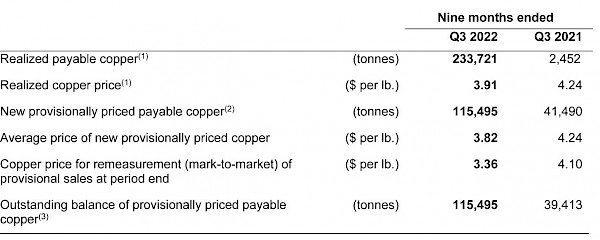

Kamoa-Kakula sold 231,525 tonnes of payable copper in nine months ended September 30, 2022, realizing revenue of $1,474.2 million for the Kamoa Holding joint venture, compared to 41,490 tonnes of payable copper sold realizing revenue of $342.6 million in Q3 2021. Revenue did not increase in proportion to tonnes sold due to the lower prevailing copper price in Q3 2022. The realized, provisional and copper price used for the production remeasurement (mark-to-market) of provisional sales can be summarized as follows:

(1) Payable copper that was provisionally priced in prior or current periods and settled during the period.

(2) Provisionally priced payable copper sold during the period is subject to final pricing over the next several months.

(3) Outstanding balance is made up of new provisionally priced payable copper from the current period that has not been realized.

The company recognized a gain on fair valuation of the embedded derivative financial liability of $89.5 million for the nine months ended September 30, 2022 (Q3 2022: loss of $27.7 million; Q2 2022: gain of $183.6 million; Q1 2022: loss of $66.4 million), compared to a loss on fair valuation of the embedded derivative financial liability of $5.2 million for the same period in 2021.

With the agreement of the development plan by the shareholders of Kipushi and the approval of the development budget consistent with the Kipushi 2022 Feasibility Study in June 2022, it was deemed probable that future taxable profit will be available from the Kipushi Project, against which the unused tax losses and unused tax credits can be utilized. As a result, the company recognized the previously unrecognized deferred tax asset in June 2022, resulting in a deferred tax recovery (income) of $112.8 million in Q2 2022.

Finance income for the nine months ended September 30, 2022, amounted to $116.8 million and was $42.5 million more than for the same period in 2021 ($74.3 million). Included in finance income is the interest earned on loans to the Kamoa Holding joint venture to fund operations that amounted to $104.0 million for the nine months ended September 30, 2022, and $68.4 million for the same period in 2021. Interest increased due to the higher accumulated loan balance and increased interest rates.

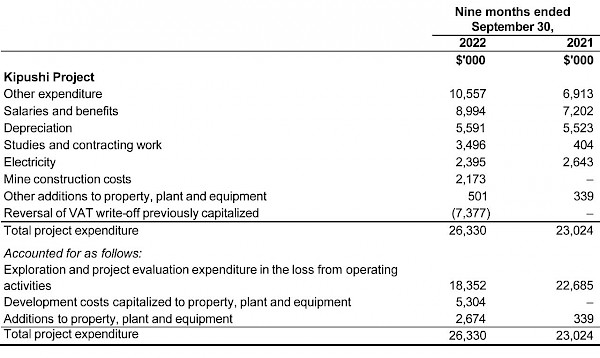

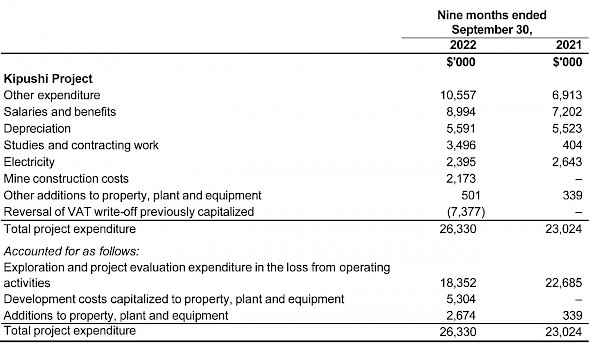

Exploration and project evaluation expenditure amounted to $30.0 million in the nine months that ended September 30, 2022, and $36.4 million for the same period in 2021. Exploration and project evaluation expenditure related to exploration at Ivanhoe’s Western Foreland exploration licences and amounts spent at the Kipushi Project until June 2022 when project development recommenced. The main classes of expenditure at the Kipushi Project in the nine months that ended September 30, 2022, and for the same period in 2021 are set out in the following table:

Financial positionas atSeptember 30, 2022, vs. December 31, 2021

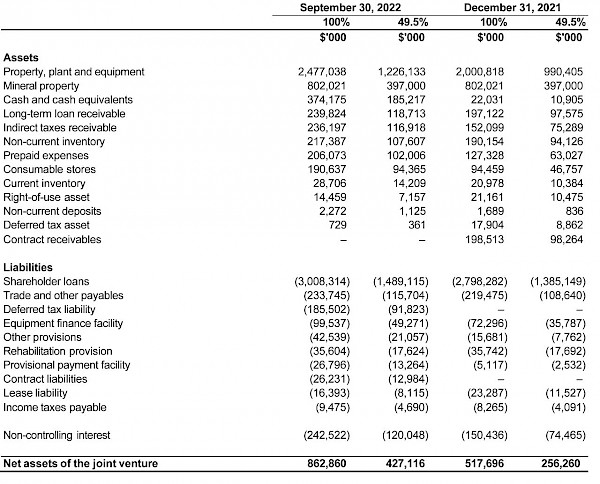

The company’s total assets increased by $555.3 million, from $3,218.2 million as at December 31, 2021, to $3,773.5 million as at September 30, 2022. The main reason for the increase in total assets was attributable to the increase in the company’s investment in the Kamoa Holding joint venture by $274.9 million, as well as the increase in deferred tax assets by $142.9 million.

The company’s investment in the Kamoa Holding joint venture increased from $1,641.8 million as at December 31, 2021, to $1,916.7 million as at September 30, 2022. The company’s share of profit from the Kamoa Holding joint venture for the nine months ended September 30, 2022, amounted to $170.9 million, while the interest on the loan to the joint venture amounted to $104.0 million. The company’s investment in the Kamoa Holding joint venture can be broken down as follows:

Before commencing commercial production in July 2021, the Kamoa Holding joint venture principally used loans advanced to it by its shareholders to advance the Kamoa-Kakula Mining Complex through investing in development costs and other property, plant and equipment.

The net assets of the Kamoa Holding joint venture, and the company’s share thereof, can be broken down as follows:

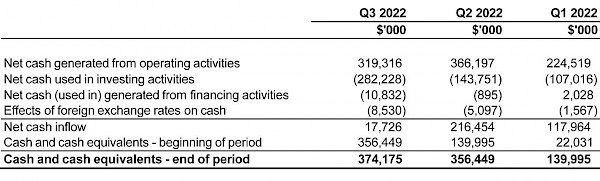

Going forward, all Phase 1 and Phase 2 operating costs and Phase 3 capital expenditures are expected to be funded from copper sales and additional facilities at the Kamoa Holding joint venture level. Cash flows generated and used by the Kamoa Holding joint venture can be summarized as follows:

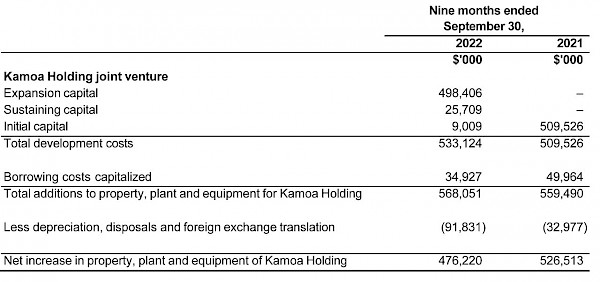

The Kamoa Holding joint venture’s net increase in property, plant and equipment from December 31, 2021, to September 30, 2022, amounted to $476.2 million and can be further broken down as follows:

Ivanhoe’s cash and cash equivalents increased by $55.1 million, from $608.2 million as at December 31, 2021, to $663.3 million as at September 30, 2022. The company spent $81.0 million on project development and acquiring other property, plant and equipment and generated $168.1 million from operating activities, which includes the receipt of the second and final prepayment of $225 million under the Ivanplats stream financing agreements. The company also invested $13.3 million in acquiring a strategic equity stake in Renergen Ltd., a South African emerging energy and helium producer. The company have however elected not to exercise its option to further increase its equity stake in Renergen.

The increase in the company’s deferred tax asset is related mainly to the recognition of the previously unrecognized deferred tax asset of the Kipushi Project in June 2022, due to the agreement of the development plan by the shareholders of Kipushi, making it probable that future taxable profit will be available from the Kipushi Project, against which the unused tax losses and unused tax credits can be utilized.

Ivanhoe’s total liabilities increased by $148.2 million to $989.4 million as at September 30, 2022, from $841.2 million as at December 31, 2021, with the increase mainly due to the deferred revenue recognized on the streaming facility of $224.0 million after transaction costs. The deferred revenue represents the prepayment for the future sale of refined gold and palladium and platinum to be delivered by the Platreef Project in the future and will be amortized as ounces are delivered to the stream purchasers.

The net increase in property, plant and equipment amounted to $46.8 million, with additions of $90.8 million to project development and other property, plant and equipment. Of this total, $74.1 million and $15.4 million, pertained to development costs and other acquisitions of property, plant and equipment at the Platreef Project and Kipushi Project respectively.

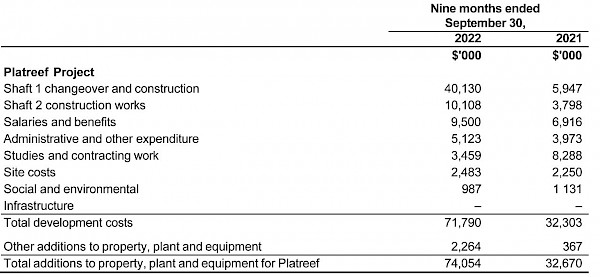

The main components of the additions to property, plant and equipment – including capitalized development costs – at the Platreef Project for the nine months ended September 30, 2022, and for the same period in 2021, are set out in the following table:

Costs incurred at the Platreef Project are deemed necessary to bring the project to commercial production and are therefore capitalized as property, plant and equipment.

The main components of the expenditure at the Kipushi Project for the nine months ended September 30, 2022, and for the same period in 2021, are set out in the following table:

Accounting for the convertible notes closed in March 2021

The company closed a private placement offering of $575.0 million of 2.50% convertible senior notes maturing in 2026 on March 17, 2021. Upon conversion, the convertible notes may be settled, at the company’s election, in cash, common shares or a combination thereof. Due to this election right and conversion feature, the convertible notes have an embedded derivative liability that is measured at fair value with changes in value being recorded in profit or loss, as well as the host loan that is accounted for at amortized cost.

The convertible senior notes are senior unsecured obligations of the company, which will accrue interest payable semi-annually in arrears at a rate of 2.50% per annum and will mature on April 15, 2026, unless earlier repurchased, redeemed or converted. The initial conversion rate of the notes is 134.5682 Class A common shares of the company per $1,000 principal amount of notes or an initial conversion price of approximately $7.43 per common share.

Holders of the notes may convert the notes, at their option, in integral multiples of $1,000 principal amount, or in excess thereof, at any time until the close of business on the business day immediately preceding October 15, 2025, but only under the following circumstances:

During any calendar quarter commencing after the calendar quarter ending on June 30, 2021 (and only during such calendar quarter), if the last reported sale price of the company’s Class A common shares for at least 20 trading days (whether consecutive) during a period of 30 consecutive trading days ending on, and including, the last trading day of the immediately preceding calendar quarter is greater than or equal to 130% of the conversion price on each applicable trading day; or

- During the five consecutive business day period after any ten consecutive trading day period (the “measurement period”) in which the trading price per $1,000 principal amount of notes for each trading day of the measurement period was less than 98% of the product of the last reported sale price of the company’s Class A common shares and the conversion rate on each such trading day; or

- If the company calls any or all the notes for redemption in certain circumstances or upon the occurrence of certain corporate events.

On or after October 15, 2025, until the close of business on the second scheduled trading day immediately preceding the maturity date, holders may convert all or any portion of their notes, in multiples of $1,000 principal amount, at the option of the holder regardless of the foregoing conditions.

The convertible notes will not be redeemable at the company’s option before April 22, 2024, except upon the occurrence of certain tax law changes. On or after April 22, 2024, and on or before the 41st scheduled trading day immediately preceding the maturity date, the notes will be redeemable at the company’s option if the last reported sale price of the company’s common shares has been at least 130% of the conversion price then in effect for at least 20 trading days (whether or not consecutive) during any 30 consecutive trading day period (including the last trading day of such period) ending on, and including, the trading day immediately preceding the date on which the company provides notice of redemption at a redemption price equal to 100% of the principal amount of the convertible notes to be redeemed, plus accrued and unpaid interest to, but excluding the redemption date.

Since upon conversion, the notes may be settled, at the company’s election, in cash, common shares or a combination thereof, the conversion feature is an embedded derivative liability. The effect of this is that the host liability will be accounted for at amortized cost, with an embedded derivative liability being measured at fair value with changes in value being recorded in profit or loss.

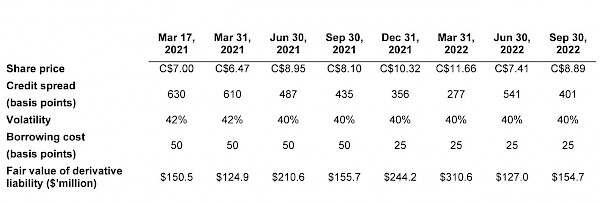

The effective interest rate of the host liability was deemed to be 9.39% and the interest recognized on the convertible notes amounted to $10.1 million in Q3 2022, after the capitalization of $0.7 million borrowing costs. The carrying value of the host liability was $461.6 million as at September 30, 2022, up from $437.4 million as at December 31, 2021.

The embedded derivative liability had a fair value of $150.5 million on the closure of the convertible notes offering and increased to $244.2 million as at December 31, 2021, and decreased to $154.7 million as at September 30, 2022, resulting in a gain on fair valuation of embedded derivative liability of $89.5 million for the nine months ended September 30, 2022. The change in the fair value of the embedded derivative liability is largely due to the changes in the closing share price of the company’s common shares at the different reporting dates.

The following key inputs and assumptions were used in determining the fair value of the embedded derivative liability:

Transaction costs on the convertible notes offering relating to the embedded derivative liability amounted to $3.7 million and were expensed and included in the profit and loss for Q1 2021.

Liquidity and Capital Resources

The company had $663.3 million in cash and cash equivalents as at September 30, 2022. At this date, the company had consolidated working capital of approximately $685.7 million, compared to $654.8 million as at December 31, 2021.

The Platreef Project entered a gold, palladium and platinum stream financing in December 2021 that will fund a large portion of the Phase 1 capital costs. The stream facilities are a prepaid forward sale of refined metals, with prepayments totaling $300 million, available in two tranches with the first prepayment of $75 million received in December 2021 following the closing of the transaction and the second prepayment of $225 million received in September 2022.

Kipushi Holding together with Gécamines, approved the development budget for the Kipushi Project in line with the Kipushi 2022 Feasibility Study and project execution is now underway. Orders for many long-lead items of equipment have already been placed and earthworks have started. Financing and offtake discussions are well advanced with several interested parties.

The company’s main objectives for the remainder of 2022 at the Platreef Project are the continued development of the project towards the completion of its first phase currently scheduled for Q3 2024, as well as the continuation of the construction of Shaft 2.

With Phase 1 and Phase 2 commercial production achieved at the Kamoa-Kakula Mining Complex, the current focus is on operational efficiency and de-bottlenecking the Phase 1 and 2 operations, as well as progressing the Phase 3 expansion.

The company has forecast to spend $72 million on further development at the Platreef Project; $49 million on development at the Kipushi Project; and $12 million on corporate overheads for the remainder of 2022. Exploration activities include a budget of $12 million on Western Forelands and $5 million on other targets for the remainder of 2022.

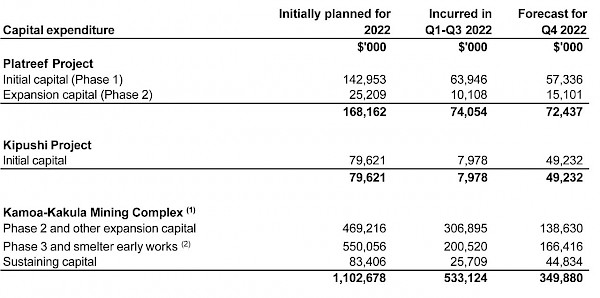

The planned capital expenditure for 2022 can be broken down as follows:

Notes: (1) Amounts in the above table for the Kamoa-Kakula Mining Complex are on a 100%-project basis. (2) The amount for Phase 3 and smelter early works are the planned expenditure for 2022 only and will be augmented on completion of the updated pre-feasibility study.

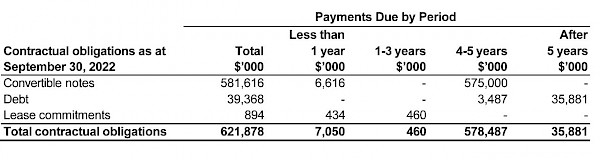

On March 17, 2021, the company closed a private placement offering of $575 million of 2.50% convertible senior notes maturing in 2026. The convertible senior notes are senior unsecured obligations of the company which will accrue interest payable semi-annually in arrears at a rate of 2.50% per annum and will mature on April 15, 2026, unless earlier repurchased, redeemed or converted. The notes will be convertible at the option of holders, before the close of business on the business day immediately preceding October 15, 2025, only under certain circumstances and during certain periods, and thereafter, at any time until the close of business on the second scheduled trading day immediately preceding the maturity date. Upon conversion, the notes may be settled, at the company’s election, in cash, common shares or a combination thereof. The carrying value of the host liability was $461.6 million and the fair value of the embedded derivative liability was $154.7 million as at September 30, 2022.

The company has a mortgage bond outstanding on its offices in London, United Kingdom, of £3.2 million ($3.5 million). The bond is fully repayable on August 28, 2025, secured by the property, and incurs interest at a rate of GBP 1-month LIBOR plus 1.9% payable monthly in arrears. Only interest will be payable until maturity.

In 2013, the company became a party to a loan payable to ITC Platinum Development Limited, which had a carrying value of $36.0 million as at September 30, 2022, and a contractual amount due of $35.8 million. The loan is repayable once the Platreef Project has residual cash flow, which is defined in the loan agreement as gross revenue generated by the Platreef Project, less all operating costs attributable thereto, including all mining development and operating costs. The loan incurs interest of USD 3-month LIBOR plus 2% calculated monthly in arrears. Interest is not compounded. The difference of $0.2 million between the contractual amount due and the carrying value of the loan is the benefit derived from the low-interest loan.

The company has an implied commitment in terms of spending on work programs submitted to regulatory bodies to maintain the good standing of exploration and exploitation permits at its mineral properties. The following table sets forth the company’s long-term obligations:

The debt in the above table represents the mortgage bond owing to Citibank and the loan payable to ITC Platinum Development Limited, as described above.

The company is required to fund its Kamoa Holding joint venture in an amount equivalent to its proportionate shareholding interest.

Non-GAAP Financial Performance Measures

Kamoa-Kakula’s C1 cash costs and C1 cash costs per pound

C1 cash costs and C1 cash costs per pound are non-GAAP financial measures. These are disclosed to enable investors to better understand the performance of Kamoa-Kakula in comparison to other copper producers who present results on a similar basis.

C1 cash costs are prepared on a basis consistent with the industry standard definitions by Wood Mackenzie cost guidelines but are not measures recognized under IFRS. In calculating the C1 cash cost, the costs are measured on the same basis as the company’s share of profit from the Kamoa Holding joint venture that is contained in the financial statements. C1 cash costs are used by management to evaluate operating performance and include all direct mining, processing, and general and administrative costs. Smelter charges and freight deductions on sales to the final port of destination, which are recognized as a component of sales revenues, are added to C1 cash cost to arrive at an approximate cost of finished metal. C1 cash costs and C1 cash costs per pound exclude royalties and production taxes and non-routine charges as they are not direct production costs.

Reconciliation of Kamoa-Kakula’s cost of sales to C1 cash costs, including on a per pound basis:

All the figures above are on a 100% basis.

EBITDA and EBITDA margin

EBITDA is a non-GAAP financial measure, which excludes income tax, finance costs, finance income and depreciation from net profit.

Ivanhoe believes that Kamoa-Kakula’s EBITDA is a valuable indicator of the mine’s ability to generate liquidity by producing operating cash flow to fund its working capital needs, service debt obligations, fund capital expenditures and distribute cash to its shareholders. EBITDA also is frequently used by investors and analysts for valuation purposes. EBITDA is intended to provide additional information to investors and analysts and does not have any standardized definition under IFRS and should not be considered in isolation or as a substitute for measures of performance prepared per IFRS. EBITDA excludes the impact of cash costs of financing activities and taxes, and the effects of changes in operating working capital balances, and therefore are not necessarily indicative of operating profit or cash flow from operations as determined under IFRS. Other companies may calculate EBITDA differently.

The EBITDA margin is an indicator of Kamoa-Kakula’s overall health and denotes its profitability, which is calculated by dividing EBITDA by revenue. The EBITDA margin is intended to provide additional information to investors and analysts, does not have any standardized definition under IFRS, and should not be considered in isolation, or as a substitute, for measures of performance prepared per IFRS.

Reconciliation of profit after tax to EBITDA:

All figures above are for the Kamoa Holding joint venture on a 100% basis.

Qualified Persons

Disclosures of a scientific or technical nature in this news release regarding the Kamoa-Kakula Mining Complex (other than stockpiles estimation), the Platreef Project and the Kipushi Project have been reviewed and approved by Steve Amos, who is considered, by virtue of his education, experience and professional association, a Qualified Person under the terms of NI 43-101. Mr. Amos is not considered independent under NI 43-101 as he is the Executive Vice President, Projects, at Ivanhoe Mines. Mr. Amos has verified the technical data related to the foregoing disclosed in this news release.